Financial Analysis for Marketers

It’s not a contradiction in terms

Many people in marketing (and product management, brand management, or business development roles) have little background in finance and accounting. Even if you have a business degree, accounting may have been long ago, and of course many people enter these roles through other educational and career paths.

As someone who teaches business for a living, I’d argue this is career-limiting. You may be able to get away without understanding money in specialized roles, but as you progress in or grow an organization, you are much better off if you understand how what you do relates to the financial concerns of the larger entity. At a basic level, someone who can demonstrate this understanding is more valuable to an organization than someone who cannot.

You will also make better decisions.

Here is my attempt to explain (some of) the jargon and help you think through (some of) the issues. Note I will be grossly simplifying issues that whole books are written about.

I’ll start with how we make money, move to how we report making money (not the same thing) and finish with some useful calculations that managers can make.

Making Money

What is Revenue?

Revenue is simply the total dollar (or euro, or yen) value of the goods (e.g., selling jam) or services (e.g., selling haircuts) that a company sells to its customers. At a simple level, think of it as the number of units of something we sell times the price we earn per unit.

Revenue is sometimes called “sales,” but I’m going to use revenue throughout this article as sales can be expressed in both units and value (e.g., dollars). (Be sure you know what the “sales” label means in any chart you read.)

Revenue is probably the single most common number by which marketers are judged. And when you hear about trendy job titles like Chief Growth Officer or growth hacker, they are almost always being asked to grow revenue.

Revenue sits at the top of an accounting statement called the Income Statement, which records revenues, costs, and profits for a specified time period. When you hear the phrase “top-line growth,” what this means is growing the revenue figure at the top of the income statement.

Two Paths to “Profit”

We make money when our revenues exceed our costs. But costs turn out to be much more complicated than revenue; a lot of financial reporting involves accountants figuring out how to best allocate costs to revenues in a given time period, and that may or may not completely match the economics of our business. There are, then, two ways of thinking about how we get to profit, the path to actual profit, and the path to accounting profit, as follows:

How We Make Money

Review: we make money when our revenues exceed our costs! Practically speaking, that means it’s critical to understand the structure of your organization’s costs. In particular, it’s important to relate revenues to an organization’s variable and fixed costs.

Variable Costs

Variable costs vary with the volume we sell. So, if we sell a jar of jam, there is the cost of the jar, the lid, the label, and the fruit, and the cost of labor of producing and packaging the jam. Every jar we make incurs more costs. If selling a unit incurs a cost, that cost is variable. Direct (hourly) labor usually falls in this category, as do materials.

Fixed Costs

Unsurprisingly, fixed costs are fixed across a range of volumes. So if we lease a building in which to make our jam, we owe our lease payment regardless of how much jam we sell. Most salaries are fixed as well, e.g., if we employ a salaried accountant to prepare financial statements, that salary is fixed regardless of how much jam we sell.

Marketing costs may be variable or fixed. If we run a $100 million TV ad campaign, that money is spent regardless of the volume generated. If we have an affiliate marketing program, on the other hand, the affiliate earns a commission on every sale. The salary portion of a sales force expense is fixed, while the commission portion is variable.

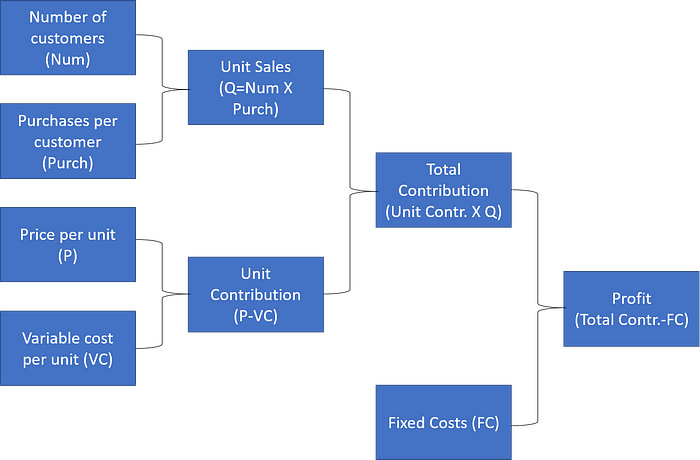

The Arithmetic of Profit

Once we understand our fixed and variable costs, we can start understanding much more specifically how we make money. Here is a summary diagram:

Let’s work backwards.

An organization makes a profit when its total contribution from unit sales exceeds its fixed costs. So if we have $1,000 in fixed costs, we need a total contribution of at least $1,000 to cover those costs and produce a profit.

Our total contribution is the product of the number of units we sell times the contribution we earn per unit. The latter is also sometimes called the unit margin or the contribution margin per unit.

Suppose our selling price is $100 and our unit variable cost is $80. This equals a unit contribution of $20. If we sell 51 units at $20 unit contribution, we have a total contribution of $1,020. Minus a fixed cost of $1,000, we have a profit of $20.

Moving all the way to the left, we then have four levers to improve total contribution:

Increase the number of customers. How can we help?

· Increase market share within the existing market (competitors’ customers)

· Expand the size of the existing market (customers not in the category)

· Expand to new markets (take your existing offer to new markets)

Increase the number of purchases per customer. How can we help?

· Cultivating more usage per usage occasion

· Increase the number of existing usage occasions

· Encourage new usage occasions for existing offers

· Cross-sell new offers to existing customers

Increase the (realized) price per unit. How can we help?

· Increase prices

· Discount less

· Upsell to more premium offers or bundles

· Negotiate lower distribution margins

· Shift to channels with lower distribution margins

· Shift to customers with a higher willingness to pay

Reduce the variable cost per unit. How can we help?

· Reduce production costs

· Identify offer attributes that may be eliminated

· Identify ways the internal production process might be streamlined

· Explore outsourcing of production

· Negotiate lower supply costs

· Look for alternate supply sources

· Reduce marketing costs

· Identify aspects of the customer journey that could be de-emphasized

· Identify ways the customer acquisition and retention processes could be streamlined

· Explore outsourcing of operations

· Negotiate lower partner costs

· Look for alternate partners

· Shift to less expensive acquisition channels

· Shift to customers with a lower cost to serve

And of course, lower fixed costs would be nice. As with variable costs, we should think about both production and marketing costs. For example, in a service business we might look at less expensive or fewer facilities. In marketing, are there ways to lower any fixed costs of customer acquisition or service?

This is the arithmetic of profit, but actual profit results from our context and decisions. First, some of these levers may be more effective or easier to implement than others in your business. Second, we need to be wary of pushing one lever and unintentionally affecting another one. We don’t want to cut costs, for example, in a way that has an outsize negative effect on unit sales.

You or your department may not control all of the levers above, but changing the ones you do and influencing the ones you don’t can be an effective way of increasing the financial success of your organization.

How We Report Making Money

You may be wondering why you need to understand reporting profit as long as you understand profit. There are three reasons.

1. Financial reporting in the form of accounting statements is critical to your senior management and finance function in communicating profit to investors, owners, regulators, and other stakeholders. You want to know how what you do changes those statements. (So do they.)

2. Financial statements can be very useful in analyzing industry or competitor profitability. The more you know about them, the better the analysis you can do.

3. The way accountants classify costs can teach us things about our business that a division between fixed and variable costs does not always illustrate.

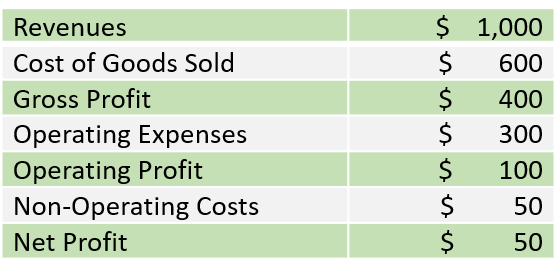

Earlier I mentioned an “Income Statement.” This is sometimes called the Profit and Loss Statement, Statement of Operations, or Earnings Statement as well, but regardless of the name it’s the primary statement by which accountants report profitability in a period.

Here is a very simple income statement for a business. Revenue sits on our top line, and then various costs and profits appear below.

Let me define some terms here.

Cost of Goods Sold (COGS; also called Cost of Services for service businesses)

This is the total cost of providing your good or service to the customer, what I called the “Cost of Producing Offer” in the paths to profit diagram earlier. So if we are selling jars of jam, what is the cost of manufacturing those jars? This would typically include the materials (e.g., ingredients, jars), labor (who makes the jam), and costs related to manufacturing (e.g., providing power to the manufacturing facility). Note that some of these costs will likely be fixed and some variable (thus the dashed lines in my paths to profit diagram).

Gross Profit

Gross Profit = Revenue minus COGS.

This is also sometimes called Gross Margin, but be wary of this label, as it can mean either the dollar value of gross profit or the percentage of revenues that gross profit represents. As with “sales,” be sure you know what “gross margin” means in any table or chart you read.

At a basic level, gross profit tells us whether our offering is a good idea. If we cannot command sufficient revenues to offset the cost of producing our offering, this suggests we are either economically unviable or a charitable organization that must rely on “the kindness of strangers” (donors, or for some startups, investors). Positive gross profits suggest an idea that is worth supporting. And why would you spend money supporting something that you can’t make money on?

Note it may be perfectly reasonable for gross profit to be negative in the short run if there is a path to profit in the long run. For example, go back to fixed and variable costs: especially early in a company’s life, it may not yet make enough money to cover its fixed production costs. Think about a small business that starts a bus route. For a given route, every bus leaving the station is a fixed cost of equipment (the bus) and personnel (the driver). If initially very few riders are interested, the route will not be profitable, but increasing ridership will eventually generate enough revenue to cover the fixed costs and “breakeven,” a calculation I’ll discuss in the final section.

Operating Expenses (or Operating Costs)

These are all the costs of managing the business that are separate from the production of the offer. This is what I called the “Cost of Supporting Offer” in the paths to profit diagram. Marketing, for example, is an operating expense. So is compensation for people in Human Resources, Sales, IT, R&D, and Finance. The cost of non-production facilities such as corporate headquarters also constitute an operating expense. Sometimes this will be lumped into a single line item called “SG&A,” which stands for Sales, General, and Administrative expenses. And as with COGS, some of these may be fixed costs and some variable.

Operating Profit

Operating Profit = Gross Profit minus Operating Expenses.

As with gross profit, this is sometimes called operating margin — the same labeling caveat under gross profit applies here. It is also sometimes labeled EBIT for Earnings before Interest and Taxes.

Operating profit reflects the larger quality of management as a whole. Given we have a good idea (positive gross profit), how well are we supporting that good idea? Extravagant spending on a corporate headquarters or moonshot R&D projects, for example, may detract from an otherwise viable business. And even when managed well, sometimes we find the cost of supporting the offer (e.g., marketing) is higher than the value added commanded in the marketplace.

For most managers in charge of a product line, account, or offering, revenues, gross profit, and operating profit are the big income statement measures to track over time.

What’s Net Profit Then?

Net profit (or net income or net earnings) = Operating Profit minus non-operating costs.

A business may incur costs that have nothing to do with operations. For example, when we borrow money, we owe interest back on this financing. This is a financing cost, not an operating cost. Similarly, we have to pay taxes, which are not operating expenses. We may also incur one-time charges when we sell an asset at a profit or a loss. Most line marketing and product managers do not need to worry about these on an everyday basis, but senior management and finance care deeply about these as they tell us something about the ultimate return to owners and investors.

Accounting Profit ≠ Profit ≠ Cash

Finally, I suggested earlier that accounting profit may not equal economic profit. Nor may it indicate how much cash we have in the bank. That is because accountants apply specific rules and guidelines to report profits, and some of the expenses reported may vary from reality. Beyond the scope of this article, this is often due to how we allocate revenues and costs across time. So when we book a sale may not be when we get paid, and when we buy an asset (like the bus I mentioned earlier), how we allocate the expense of the bus is a judgment. The important thing is that the Income Statement is an estimate of the true profitability of a business in a time period, and we can learn from it. Take an accounting course or try the Financial Intelligence book in the references for more. Or maybe make a friend in your accounting department!

Useful Calculations

Finally, a couple of areas where simple arithmetic can be useful.

Margins and Markups

Using percentages to calculate the profit margins of various parts of your economic system can be extraordinarily helpful. Percentages make it easy to compare across different sizes of businesses or business units.

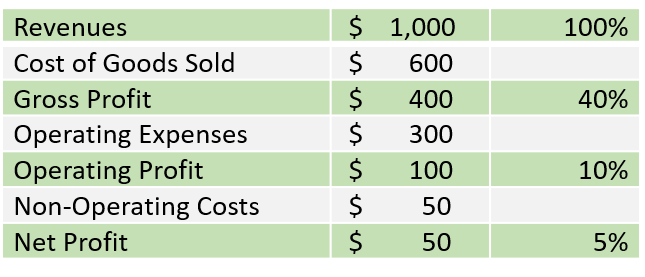

Three common ratios are calculated directly from the income statement, as follows.

Gross Profit Margin = Gross Profit/Revenue

This tells you what percentage of the revenue you earn is realized in gross profit. Small gross margins mean that you are commanding a very small premium over your cost of production. Large gross margins suggest that your offering is highly valued relative to its costs.

Operating Profit Margin = Operating Profit/Revenue

This is the same calculation as we make for Gross Profit Margin, but here it tells us how profitably we manage the operation as a whole.

Ad/Sales Ratio = Advertising Expenditure/Revenue

This is a common metric looking at the efficiency with which advertising (or marketing for a marketing:sales ratio) is generating sales. So if we spend $100 in advertising and generate $1,000 in revenues, we have an ad/sales ratio of 10%, meaning we are spending about ten cents for every dollar in sales we earn. This ratio is often used in advertising budgeting (which may not be the best idea).

Here is the income statement I showed you earlier with the gross, operating, and net margins:

Numbers without context are meaningless. For the income statement ratios, two useful contexts are the past and competition.

To the extent that your profit margins are changing over time, that means your revenues are not growing at the same rate as your costs. If your gross profit margins are going down over time, this means your production costs are growing more quickly than your revenues, which is an unhappy situation unless temporary.

Competitively, comparing to the averages or norms for your industry or key competitors can be helpful. If your industry “typically” has operating margins that are less than yours, that suggests you have some kind of advantage. What is it?

Margins and their calculation cousin, markups, are also often used when calculating prices and distribution profits. Usually when we talk about margins, it is as a percentage of sales as I calculated earlier in this section. Markups, on the other hand, are calculated as a percentage of costs, though you should be careful to understand what is being calculated in a given situation as some people use the terms loosely.

In pricing, a common (though rarely optimal) method is to calculate “cost plus” prices. In this case, the “plus” is a markup on the cost. So if a product costs $80 to manufacture and we mark that up to a price of $100, that is a markup of 25% ($20/$80). If we calculate instead a margin, $20/$100 would be 20%. Companies may have specific margin or markup goals they seek in their products.

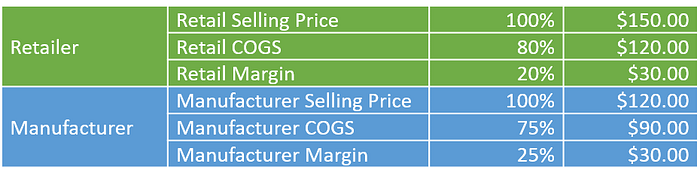

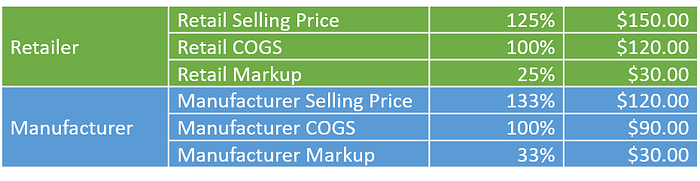

For distribution channels, distributors perform a variety of functions for their suppliers, and for that they receive a profit margin. Imagine, for example, that we are a microwave oven manufacturer using a retailer to sell our ovens. We spend $90 to manufacture an oven that we sell to the retailer for $120. The retailer in turn sells that oven to a consumer for $150. Here is what the margins look like.

Retail Margin example

The retailer receives a margin of 20% ($30) for the services it performs for us. This is the retailer’s gross margin, from which it must subtract its operating costs. The Retail COGS here is the same as our manufacturer selling price, because it buys the oven from us for $120.

Here is the same table, this time using percentages marked up on cost:

Retail Markup example

As you can see, the dollar figures are identical, but the percentages vary depending on whether we use margins or markups.

One of the things we learn from tables like this is the total distribution system profit. If the consumer buys the product for $150 and we produce it for $90, that means there is a total of $60 in profit to split across the system. In the example, the retailer and we each receive $30 to cover operating costs. This may or may not be an equitable distribution.

When you hear manufacturers say they will save consumers money by “cutting out the middleman,” the manufacturer is looking at that $30 the retailer gets. If we distributed directly to consumers, conceivably we could cut the price to $130. We would realize a $40 profit margin rather than $30, while the consumer would save $20. But this only works if we can perform the necessary distribution tasks for $10 ($40 — $30 manufacturing cost)!

Breakevens

A final financial calculation that is very helpful in planning is to calculate the breakeven on the fixed costs of an initiative. This relates to the analysis of fixed and variable costs I discussed earlier. For a business to be profitable, it must sell enough units at a positive unit contribution to cover its fixed costs. How many units is that? A breakeven calculation tells us the answer.

Suppose the total launch costs to get a new product out the door is $10 million. How many units do we have to sell of the product to cover that $10 million fixed cost?

The formula for a breakeven is as follows:

The unit contribution is exactly what we calculated earlier: price minus variable costs.

In this case, if our contribution per unit is $10, then we need to sell 1 million units to cover the $10 million fixed cost of the launch.

The managerial question is whether that is a big number. If 1 million units is very daunting, we might want to revisit either our launch costs or our unit contribution structure.

How do we decide that? One common way is to look at what percentage of the market (market share) the breakeven volume represents. So if the market now sells about 2 million units, 1 million represents a 50% market share. That’s a big number. Even if we can capture a full 50% of the market, how long will it take? On the other hand, if the market currently sells 100 million units, a 1% market share may feel achievable.

For a new market, the market penetration rate fulfills a similar function. What percentage of the potential market do we have to sell to (“penetrate”) to cover our fixed costs? If we think the potential market is 2 million units, 50% would be daunting. If we think the potential market is 100 million units, 1% is perhaps less so.

Note you can also think about breakevens in a customer acquisition sense. If our customer acquisition cost is $100, how many units do we need to sell to that customer to cover that cost? Is that a big number. . .

I hope this article has been useful to you. I’ve given you a couple of references below in case you would like to learn more.

Bruce Clark is an Associate Professor of Marketing at the D’Amore-McKim School of Business at Northeastern University. He researches, writes, speaks, and consults on managerial decision-making, especially regarding marketing and branding strategy, customer experience, and how managers learn about their markets. You can find him on LinkedIN at https://www.linkedin.com/in/bruceclarkprof/. He is not an accountant, and has been grateful for the advice of several correspondents who helped him think through this article, including @cambartley, @neilbendle,@mdbergman36,@jonmbradshaw @jonathandunnett,@andrewceverett, @TomLewis_CPI, and @FinanceDirCFO. That doesn’t mean he did everything they said or they like how he did it. . .

References for Further Reading

Berman, Karen and Joe Knight, Financial Intelligence, Harvard Business School Press, 2006. This is a highly readable book about how to understand financial information in general. The 2006 edition is the one I have read, but they produced a second edition in 2013.

Robertson, Graham, Beloved Brands, 2020. This is a practical book on the nuts and bolts of classic FMCG brand management from a former practitioner. He includes a Marketing Finance 101 chapter with many thoughtful ideas.